Student loan debt can be a significant financial burden for many graduates, but with effective strategies, you can manage and reduce your debt over time. Proper planning, disciplined repayment, and leveraging available resources are key to minimizing the impact of student loans on your financial future. Here are some practical tips and strategies for managing and repaying student loan debt.

**1. *Understand Your Loans*

Before you can effectively manage your student loan debt, it’s essential to understand the types of loans you have, their interest rates, and the repayment terms. Start by reviewing your loan documentation and creating a detailed list of all your loans, including:

- Loan Types: Identify whether your loans are federal or private, as they have different terms and repayment options.

- Interest Rates: Note the interest rates for each loan, as they impact the total amount you’ll repay.

- Repayment Terms: Understand the length of the repayment period and any specific conditions associated with each loan.

**2. *Create a Budget and Prioritize Payments*

Developing a budget is crucial for managing your finances and ensuring timely loan payments. Include your loan payments as a fixed expense in your monthly budget. Prioritize paying off high-interest loans first to reduce the total amount of interest paid over time.

Consider using a budgeting app or spreadsheet to track your income and expenses. Allocate funds for loan payments, savings, and other essential expenses, and adjust your spending habits to ensure you stay within your budget.

**3. *Explore Repayment Options*

Federal student loans offer various repayment plans that can help you manage your payments based on your income and financial situation:

- Standard Repayment Plan: This plan offers fixed monthly payments over a set period, typically 10 years. It’s a good option if you want to pay off your loans quickly and save on interest.

- Income-Driven Repayment Plans: These plans base your monthly payments on your income and family size. Options include Income-Based Repayment (IBR), Income-Contingent Repayment (ICR), and Pay As You Earn (PAYE). These plans can lower your monthly payments but may extend the repayment period.

- Graduated Repayment Plan: Payments start lower and increase over time. This plan is suitable if you expect your income to rise significantly in the future.

For private loans, check with your lender for available repayment options, such as refinancing or extending the loan term.

**4. *Make Extra Payments*

Whenever possible, make extra payments toward your student loans. Extra payments can reduce the principal balance, which decreases the amount of interest you’ll pay over the life of the loan. Even small additional payments can make a significant difference over time.

Consider making extra payments whenever you receive a bonus, tax refund, or any unexpected income. Be sure to specify that the extra payment should be applied to the principal balance to maximize your savings.

**5. *Refinance and Consolidate*

Refinancing and consolidation can help you manage your student loans more effectively:

- Refinancing: This involves taking out a new loan with a lower interest rate to pay off your existing loans. Refinancing can reduce your monthly payments and the total interest paid. However, be cautious with federal loans, as refinancing through a private lender may result in losing federal benefits like income-driven repayment plans and loan forgiveness options.

- Consolidation: Federal student loan consolidation combines multiple federal loans into a single loan with a fixed interest rate based on the average of your current rates. This can simplify payments and extend the repayment period, but it may also result in paying more interest over time.

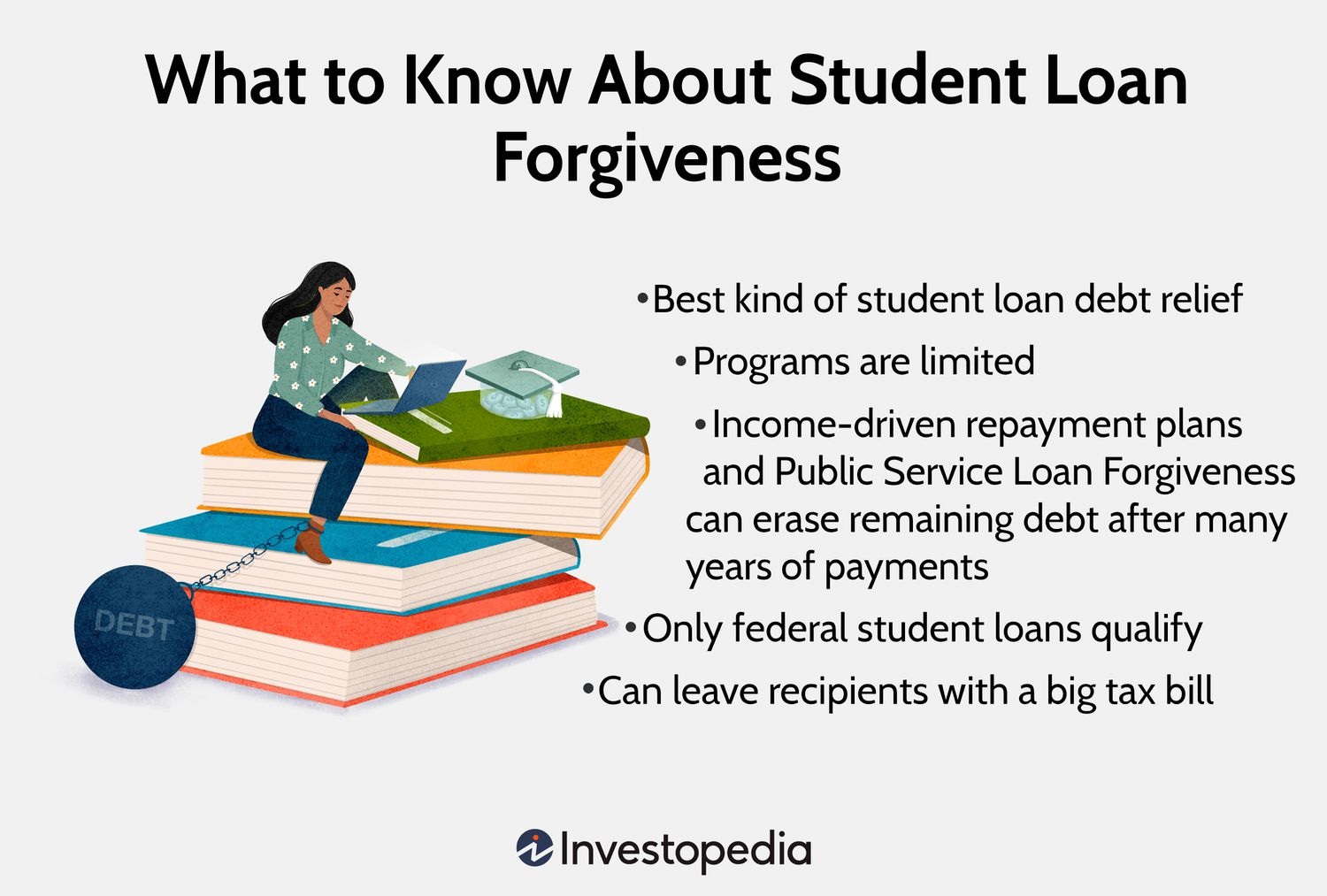

**6. *Stay Informed About Loan Forgiveness Programs*

If you work in certain fields or for specific employers, you may be eligible for loan forgiveness programs. For example, the Public Service Loan Forgiveness (PSLF) program offers forgiveness for federal loans after making 120 qualifying payments while working for a qualifying employer.

Research available loan forgiveness options and ensure you meet the eligibility requirements. Keep accurate records of your employment and payments to facilitate the forgiveness process.

**7. *Seek Financial Counseling*

If you’re struggling to manage your student loan debt, consider seeking help from a financial counselor or advisor. They can provide personalized advice on budgeting, repayment strategies, and loan management.

Conclusion

Reducing student loan debt requires proactive management and strategic planning. By understanding your loans, creating a budget, exploring repayment options, making extra payments, considering refinancing or consolidation, staying informed about forgiveness programs, and seeking professional advice, you can effectively manage and reduce your student loan debt. Implement these strategies to achieve greater financial stability and work towards a debt-free future.